Dash Cams Save The Day

Dash cams have become increasingly popular among drivers, and for good reason. In today’s driving environment, accidents can happen quickly, details can be disputed, and…

Read BlogDash cams have become increasingly popular among drivers, and for good reason. In today’s driving environment, accidents can happen quickly, details can be disputed, and…

Read Blog

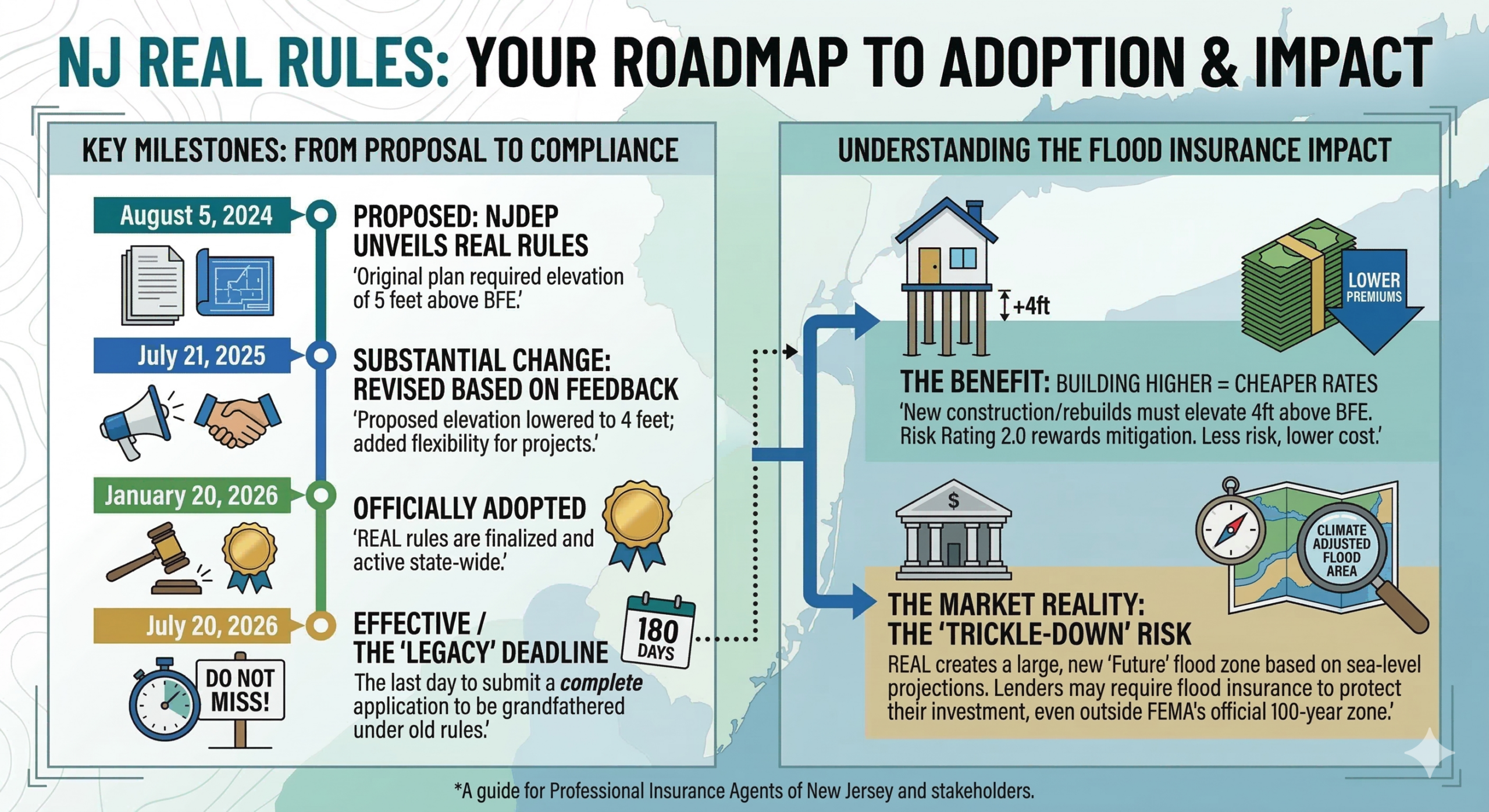

New Jersey is fundamentally changing how we develop our coastlines and manage flood risk. Spear headed by the NJDEP, the Resilient Environments And Landscapes (REAL)…

Read Blog

Workers’ compensation audits are a critical part of your business insurance program, yet they’re often misunderstood or overlooked until the end of the policy term….

Read Blog

Electric bikes have quickly become a popular way to commute, exercise, and get around town. They’re efficient, environmentally friendly, and accessible to riders of all…

Read Blog

If you own a business, you’ve probably heard the terms general liability and professional liability tossed around — sometimes interchangeably. The truth is, they cover…

Read Blog

Data breaches aren’t just something that happen to big corporations anymore. Today, personal information is leaked, sold, and exploited at an alarming rate — often…

Read Blog